Revenue Cycle

6 Best Healthcare Claims Management Software (2026 Guide)

6 Best Healthcare Claims Management Software (2026 Guide) Quick Summary Choosing the right healthcare claims management ...

Read the full article →

Navigating the complexities of insurance billing and coverage can often seem daunting for substance abuse and mental health facilities. As providers, understanding the nuances of various insurance policies is crucial for seamless operational management and guaranteeing that clients receive the care they deserve without financial hindrance. This blog aims to demystify the labyrinth of insurance terms, benefits, and claims processes. By enhancing your insurance knowledge, you can focus more on providing top-notch mental health services, confident that the administrative aspects are handled efficiently and correctly. Suppose you’re grappling with the details of billing codes or the specifics of patient eligibility. In that case, this post is designed to help your facility with the necessary insights to manage insurance interactions with poise and professionalism.

Risk means a situation involving exposure to danger, harm, or loss

Risk in terms of Insurance = the possibility of financial loss

Risk is what makes you decide whether or not you need insurance.

Risk is the key factor that insurance companies consider when deciding whether to provide you with insurance and how much it will cost. The higher the risk, the more you’ll likely to pay for insurance. This is why understanding and managing risk is crucial for insurance interactions.

Avoidance: Choosing not to participate in an activity because of the risk involved, such as golfing in a lightning storm.

Retention: Saving resources in case of future loss. E.g., storing food in preparation for a hurricane or putting money away in savings.

Transfer: Passing the risk on to someone else. E.g., Paying a monthly premium for an insurance policy and expecting the insurance company to protect your assets.

Insurance – a legal contract that guarantees compensation for specified loss, damage, illness, or death in return for payment of a premium

Policyholder – a person who pays premiums to own an insurance policy and has the privilege to exercise the rights stated in the insurance policy; also called insured, patient, subscriber

Beneficiary – the covered entity of an insurance policy. The one who receives the benefit. Could be policyholders or dependents

Patient – In substance abuse & mental health, referred to as ‘Client’. Receives services from providers for medical, mental, & addiction-related issues. Also called insured, policyholder, dependent.

Provider – A healthcare professional or facility that provides preventative, curative, promotional, or rehabilitative services to patients.

Payor – An insurance company, the responsible party for paying claims submitted by the provider for services rendered to the patient

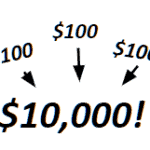

Suppose there are 100 people in a group

1%

With a 1% chance that one of them could get sick and require $10,000 in medical care

?

With a 1% chance that one of them could get sick and require $10,000 in medical care

If each person pays $100 into a “pool” they will collectively have $10,000 to cover the medical costs of the person who gets sick.

</= $100

So, everyone gives up $100, but never loses more than $100

The 1 sick person is covered for the $10,000; the rest do not collect anything, but they gain peace of mind and important protection against large loss

The 1 sick person is covered for the $10,000; the rest do not collect anything, but they gain peace of mind and important protection against large loss

Law of Large Numbers – As the number of policyholders increases, the insurance company is more confident that its prediction will prove true. Therefore, insurance companies attempt to acquire many similar policyholders who all contribute to a fund that will pay the losses.

For example, the insurance company may know that, on average, two out of 100 homes will burn in a given year, but it will be much more confident in this prediction if it insures 1,000 homes— even more confident if it insures 100,000 homes. The more chances you get, the more likely you will achieve the desired outcome.

For our purposes, we will primarily be concerned with commercial insurance.

For our purposes, we will look at health insurance coverage.

Policy – the contract specifies what risks are covered and how much will be paid for losses

Coverage – the risk covered and the amount of money paid for losses under an insurance policy

Premium – money paid to an insurance company to purchase a policy

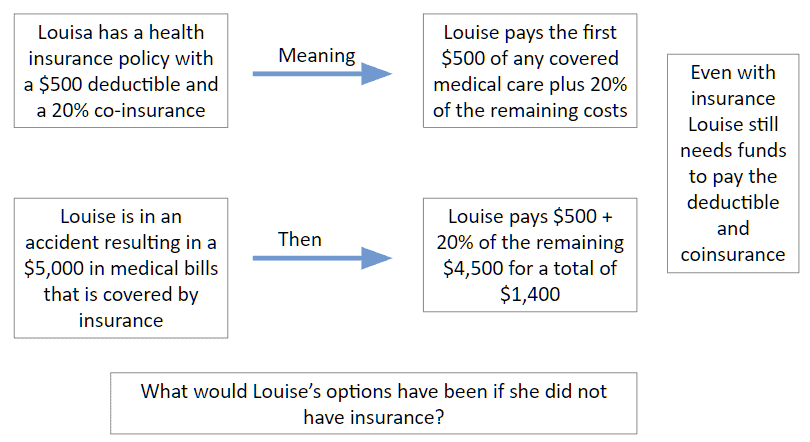

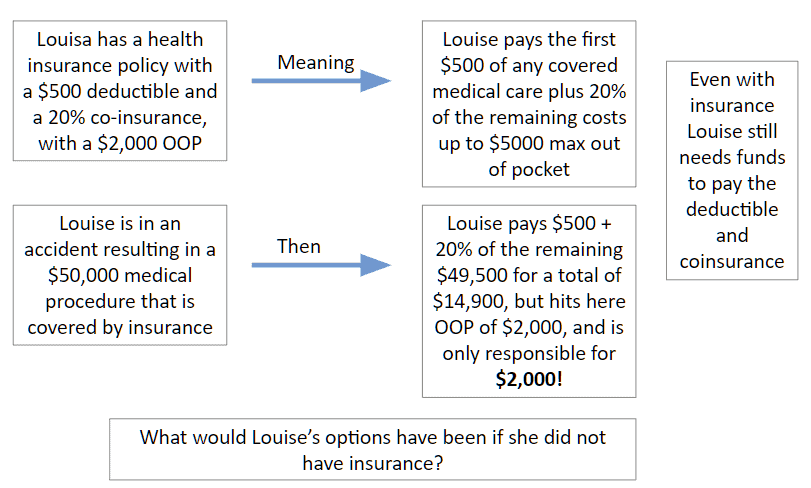

Deductible – a specified amount of money that the insured must pay before an insurance company will pay a claim

Co-pay – a payment made by a beneficiary (especially for health services) in addition to that made by an insurer

Co-insurance – the shared payment the insured pays against a claim

Limitations – the maximum amount of benefit (in dollars, days, or covered services) the insurance company will pay.

E.g., A policy with limits of $1,000,000/$3,000,000 will provide a maximum of $1M per claim and $3M for all claims during a policy term

Exclusions – anything that is specifically not covered by your insurance policy and is outlined in the Exclusions section of your plan

For example, some insurance policies may not cover sub-acute residential detox.

Accreditations Requirements – some insurance companies require the provider to be accredited by a third party to ensure quality of service and compliance for services to be covered & reimbursed (e.g., The Joint Commission, CARF)

Assignment of Benefits – Abbreviated ‘AOB’ stipulates which party (patient or provider) will be paid when the payor (insurance company) pays a claim.

Authorization Requirements – oftentimes, services require authorization from the insurance company before the patient can be treated and claims reimbursed. A Utilization Review department (abbreviated “UR”), also called Utilization Management (abbreviated “UM”), will call the insurance company to obtain authorized time (meaning, authorized services and/or days).

Using the same example, say Louisa had $50,000 in medical bills.

What would Louisa’s responsibility be?

$50,000 in bills

– $500 deductible

$49,500 remaining

20% co-insurance x $49,500 remaining = $9,900

Louisa’s responsibility = $500 deductible + $9,900 = $10,400!

To keep Louisa’s responsibility affordable, insurance has something called Maximum Out of Pocket (usually expressed as OOP Max); once Louisa reaches her OOP Max, insurance covers the remaining of her bills.

Out of Pocket Max (OOP) Example

The difference between the billed amount and the allowed amount is vital to understanding what the provider will be reimbursed and what the patient will be responsible for paying.

Allowable Amount may be established by:

Providers often accept the allowed amount and do not bill patients for any remainder.

Using Louisa’s example, with $50,000 in medical bills and $2,000 in patient responsibility, insurance determines the amount of $30,000 that is allowed by the provider.

$50,000 in bills

-$2,000 paid by Louisa

-$30,000 allowed (paid) by insurance

$18,000 remaining

Providers may “balance bill” the patient for the remainder or write this amount off as a loss.

Health Maintenance Organization (HMO) – you pick one primary care physician. All your health care services go through that doctor. That means you need a referral before seeing any other healthcare professional, except in an emergency. Visits to healthcare professionals outside your network typically aren’t covered by your insurance.

For example, you won’t go straight to a dermatologist if you get a skin rash. You would first go to your primary care physician, who‘d examine you. If your primary care physician can’t help you, he or she will refer you to a trusted dermatologist in your network who will.

One exception to this is that women don’t need a referral to see an obstetrician/gynecologist or OB/GYN in their network for routine services such as Pap tests, annual well-woman visits, and obstetrical care.

Coordinating all your health care through your primary care physician means less paperwork and lower health care costs for everyone.

Preferred Provider Organization (PPO) – also called Point of Service (POS), PPO plans give you flexibility. You don’t need a primary care physician. You can go to any healthcare professional you want without a referral—inside or outside of your network.

Staying inside your network means smaller copays and full coverage. If you choose to go outside your network, you’ll have higher out-of-pocket costs, and not all services may be covered.

Exclusive Provider Organization (EPO)—EPO plans combine the flexibility of PPO plans with the cost savings of HMO plans. You won’t need to choose a primary care physician and don’t need referrals to see a specialist.

However, you’ll have a limited network of doctors and hospitals, and EPO plans don’t cover care outside your network unless it’s an emergency.

It’s important to know who participates in your EPO plan’s network. You’ll pay all costs if you go to a doctor or hospital that doesn’t accept your plan.

Parity Act

Why is this important?

Because insurance coverage for substance abuse and mental health must be the same as the health benefit (whereas before, they could charge more or limit it more than the medical/surgical benefit)

Affordable Care Act

Pre-existing Conditions

Why is this important?

Insurance can no longer deny you care based on a previous diagnosis (substance abuse / mental health) or charge you more, and the substance abuse / mental benefit must be a covered benefit.

Navigating insurance for mental and substance abuse health facilities can be challenging. Still, with the right knowledge and strategies, it can also be managed effectively to ensure that the facility and its clients are safeguarded against undue financial risks. Providers must understand the types of insurance available, the components of insurance policies, and the legislative landscape that shapes how these policies are implemented. With this knowledge, facilities can make informed decisions that optimize their coverage and fulfill their crucial role in providing care.

Moreover, facilities should continuously be educated about changes in insurance regulations and new healthcare laws to stay compliant and up-to-date with industry standards. Implementing a robust billing system and training staff to handle insurance claims proficiently can reduce errors, minimize claim rejections, and expedite payments. Facilities must also review their policy choices regularly to ensure they get the best possible coverage at the most reasonable cost, considering new options like cyber insurance to protect against digital risks.

Understanding the detailed nuances of insurance interactions, such as the implications of co-pays, deductibles, and co-insurance, can also significantly affect the facility’s financial health and the quality of service provided to clients. By effectively managing these aspects, facilities can avoid the pitfalls of underinsurance or costly overinsurance.

Ultimately, the goal is to enhance the facility’s operational efficiency and ensure financial stability, enabling providers to continue offering essential mental health and substance abuse services to those in need. This commitment to fiscal responsibility and high-quality patient care will foster a stronger, more resilient healthcare system.

Disclaimer: All trademarks, logos, and brand names are the property of their respective owners. The use of any third-party trademarks, logos, or brand names in this article is for informational and comparative purposes only, and constitutes nominative fair use. This article was published by VerifyTreatment, and while we strive for objective comparisons, VerifyTreatment is included as an option within this list.

Samantha is a dynamic marketing professional dedicated to making a difference in the behavioral health industry through her work at VerifyTreatment. With a strong background in digital marketing and brand advocacy, she helps elevate the platform’s presence by fostering authentic connections with treatment centers and healthcare providers. Her expertise in content creation and community engagement ensures that VerifyTreatment’s value is communicated effectively, helping centers streamline operations and improve patient care. Samantha’s focus on building trust and driving awareness positions VerifyTreatment as a key resource in the healthcare landscape.

Nicole is a versatile healthcare professional with a Bachelor’s degree in Health Administration and a solid background in managing healthcare systems and operations. Her experience spans healthcare management, compliance, and regulations, making her adept at navigating complex healthcare environments. In addition to her administrative expertise, Nicole holds certifications in Functional Nutrition and Personal Training, giving her a well-rounded perspective on health and wellness. She is committed to using her skills to improve healthcare settings and ensure effective, patient-centered care.

Tara is a dedicated leader who leverages her Master's degree in Information Technology (Florida Tech) and deep company knowledge (since 2018) to drive our community awareness. She is the central figure for managing social engagement and ensuring the community is immediately and effectively informed of all new product launches and company updates.

JoAnn has a strong background in the mental health and substance abuse industry, with expertise in billing, coding, facility credentialing, and contracting. She is passionate about team education and public speaking, always striving to make a positive impact. With a solid foundation in accounting, JoAnn also holds an Associate of Arts in Biblical Studies from Liberty University, blending her professional skills with her personal values.

For 11+ years, Melanie has been dedicated to helping clients access quality mental health care, with a special focus on grief, loss, and substance abuse. With expertise in healthcare, community outreach, patient advocacy, and leadership development, Melanie is passionate about making a positive impact in the lives of others.

Jordan is a dedicated advocate for behavioral health and is passionate about improving sales strategies and business processes. With a focus on helping businesses, particularly in healthcare, Jordan believes that streamlining operations is a way to positively impact more people indirectly. A strong leader, both personally and professionally, Jordan is committed to making a difference in the world by doing good business and serving a higher purpose.